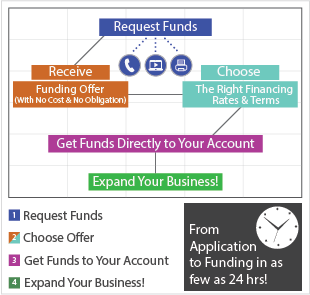

- No Collateral Required

- No Personal Guarantee

- Quick Online Application

- Flexible - Automated Payback

- No Business Plan Necessary

- Bad Credit OK

Business Unsecured Cash Advance up to $250,000!

"A" credit customers:

Customers who can obtain a loan from traditional lenders, because they have perfect credit.

Acceleration Clause:

The part of a contract that secures payments for the full term of the contract.

Account:

The total claims and/or invoices against a particular customer; how much is owed by a specific customer for goods or services rendered.

Account Debtor:

The entity (business, organization or individual) responsible for paying an invoice.

Accounts Payable:

Outstanding debt; the amount of money owed by a company for goods and services received.

Accounts Receivable:

A collection of a company's outstanding invoices (invoices which have not yet been paid by the company's customers).

Accounts Receivable Aging Report:

An internal report detailing to what extent invoices on each account have been outstanding.

Accounts Receivable Financing:

Accounts receivable based financing. Factoring is one type of accounts receivable based financing. In another type, funds owed to the client are used as collateral. financing In this instance, the funding source does not own the invoice and is not responsible for collecting the debt.

Advance Rate:

The specific percentage of the income stream advanced to a client by the party providing financing,

Amortization:

The payment of debt in installments of principal and interest for a proscribed time, at the end of which, the debt will have been paid in full. Mortgages, as well as many other loans, are paid in this gradual, systematic method.

Articles of Incorporation:

The legal document filed by the founders of a corporation with a U.S. state. Once the articles have been approved, the state issues a Certificate of Incorporation. These two documents compose the Charter of Incorporation.

Asset:

Belongings which have commercial or exchange value. Assets can be owned by a business, institution or individual. Assets might include property, machinery, inventory, intellectual assets such as copyrights or trademarks, and accounts receivable.

Asset Based Lending:

Lending where collateral, such as equipment or inventory, is used to secure the loan.

Assign ability:

The authority and ability to assign (or sell) an income stream to a separate entity.

Assignee:

The entity who is obtains the right to an asset, through gift or purchase.

Assignment:

The transfer of any debt instrument and/or it’s rights, title or interest from one party to another.

Assignor:

The party who is transferring an asset, through gift or sale, the assignor forfeits the rights to the asset which is being assigned.

Authorized Signatory:

Someone who is legally able to enter a binding contract on behalf of a business.

"B" through "D" credit customers:

Consumers with varying degrees of credit, either less-than-perfect (B) to bad (D) credit. These customers usually will not qualify for traditional financing. Another name for these customers is ‘sub-prime credit customers’

Bad Debt:

Debt which has been written off as uncollectible due to delinquency.

Balance sheet:

The accounting tool used to show the current financial condition of a business. It is a financial statement which records assets on the left side of the sheet and liabilities and net worth on the right side of the sheet.

Balloon:

The final payment of principal that is due at a specific point in time prior to the time required to fully amortize the debt. A balloon payment is generally substantially larger than previous payments.

Bankruptcy:

The state of insolvency of a legal entity that does not have the financial means to pay their incurred debts as they come due. This status is initiated via petition by creditors, or by the bankrupt entity itself.

Beneficiary:

An entity entitled to inherit assets upon death of the owner and/or receive the benefits/proceeds, of a life insurance policy, when the insured person dies.

Bill of Exchange:

A financial instrument in with the buyers signature, acknowledging debt for goods/services received.

Bill of Lading:

A document providing instructions to the shipping company, used when transporting goods.

Bill of Sale:

A legal document used for certain merchandise, to transfer the title of ownership from seller to buyer.

Blanket Assignment:

A legal transfer of accounts receivable ownership, present and future, as collateral for financing.

Break Even Point:

The scope of operation where revenues equal costs.

Broker:

An individual who pairs clients with providers. In the case of financing, a broker helps those in need of funds with various financial entities.

Business-based income streams:

Cash flow originating from another business, or a government agency.

Capital Net Worth:

Assets minus liabilities. This is the worth of all assets after all debts have been satisfied.

Cash flow:

How money enters and leaves a business or household, Money enters a business through revenues or funding; it leaves a company in the form of expenses.

Cash flow broker:

This person brokers between income stream sellers and funding sources. As a cash flow broker, they might simply offer a referral service, or they could serve as the primary liaison.

Cash flow industry:

The secondary marketplace for privately held debt. The debt can be bought, sold or brokered, helping businesses and private persons to receive assistance with the management of their cash flow needs.

Cash flow instrument:

The actual future payment or series of future payments otherwise known as a ‘debt instrument’ or an ‘income stream’..

Cash flow specialist:

This term can refer to either a buyer of debt instruments, or a cash flow broker.

Cash flow transaction:

Any time that an income stream is purchased by an outside party.

Chattel mortgage:

This mortgage is a ‘security agreement’ and is normally used when a business is sold. It is a mortgage which secures debt; a chattel mortgage is on personal property.

Chapter 11:

The Federal Bankruptcy Act which allows the debtor to remain in control of his business and operations, under supervision of a court. This is only an option as long as no new unpaid debt is accrued.

Chapter 1:

Allows businesses to restructure debt and renegotiate payment schedules..

Commercial Credit Insurance:

Insurance available to businesses which protects against large losses from delinquent accounts which are declared uncollectible.

Collateral:

An asset (real estate, a vehicle, etc.) that is pledged to secure the repayment of a loan. Collateral will be seized by the lender if the borrower defaults.

Collateral-based income streams:

When collateral is used to secure debt instruments.

Collectability:

The ability to collect accounts receivable. In the case of a funding source, accounts receivable is specific to the future income stream payments which have been purchased from a client.

Commission:

A fee paid to a broker for their services.

Concentration:

The percentage of a client's accounts receivable which is owed by a single customer. If the percentage is high, then it is considered to be a large concentration, and high risk.

Confidential Invoice Discounting:

A private agreement between a factor and its client which remains undisclosed to customers of the client.

Consumer-based income streams:

Debt instruments purchased from a private individual, as opposed to a business.

Contingency-based income streams:

Debt instruments in which there are outside factors which render the amount of the payment uncertain. With contingency-based income streams, the recipient does not necessarily have legal entitlement to the payments

Conversion:

Making a client out of a qualified prospect.

Corporation:

A legal entity, which is separate and distinct from the individuals who own it; the corporation can own property, incur debts, sue, or be sued. It is possible to become a corporation through charter of a U.S. State or the Federal Government.

Corporate Resolution:

A resolution voted on by the corporation.

Current Liabilities:

Debts that must be paid in one year, or less. Items to be found on a balance sheet under current liabilities include Accounts Receivable, Notes Payable, Bank Loans Payable, Taxes Payable, Wages, and long-term debt which is due within one year.

Credit Analysis:

The comprehensive analysis which measures the estimated creditworthiness of a potential client.

Creditor:

The person or company owed to by a debtor.

DBA (Doing Business As):

The designation (like AKA for also known as) for any non-official name the business uses.

DBT (Days Beyond Terms):

The designator for the number of days an invoice is overdue.

Debt instrument:

A debt that is owed from one party to another. The future payment(s) are also known as cash flow instruments or income streams.

Debtor:

The entity who is in debt. The debtor has borrowed, and makes payments to repay his debt to the creditor.

Default:

The non-fulfillment of a legal promise, duty, or other obligation. (e.g. to pay a debt).

Delivery Evidence:

In shipping, this document serves as proof of the delivery and invoicing of goods.

Direct Mail:

Marketing through sending advertising and solicitations to large numbers of potential customers through the mail.

Discount Factoring:

A factor (the party providing the financing) buys accounts receivable from businesses (the party receiving the financing) at a discount to the face value. The factor’s fee is dependent upon the number of days until the receivable paid.

Discount Fee:

In the case of factoring, the discount fee is dependent upon the number of days until the receivable paid. The basis of the fee is the discount rate, which is set prior to the purchase of the accounts receivable and is listed in the Discount Schedule.

Discount Rate:

In factoring, a discount rate functions similarly to an interest rate, in that it is multiplied by the number of days the receivable remains unpaid. It is the percentage discount the factor receives when purchasing a receivable.

Due diligence:

Extensive research on a business, proposal or transaction. Parties providing financing may perform credit checks, appraisals, UCC searches, lien searches or in-person interviews with clients. Due diligence can also be done on income streams and payors.

Escrow:

Assets are held in trust by a third party, while terms and conditions outlined in the escrow instructions are either completed or terminated. The completion or termination of the instructions results in the assets being returned to the original owner, or being transferred to the second party.

Face value:

The current principal balance on a debt instrument.

Factoring:

Accounts receivable financing where the funding source purchases invoices from its clients.

Fictitious name:

The legal statement which can be filed when a person uses a different name for business dealings.

Foreclosure:

The seizure of property in court for a debt that is in default.

Funding source:

An entity that purchases income streams, or otherwise provides funding to businesses.

Government-based income streams:

Accounts receivable paid by a government entity. Government-based income streams can be paid directly by a government agency, or via an insurance company.

Hypothecation:

The process of using borrowed funds to invest in a debt instrument, and using security interest in the debt instrument as the loan’s collateral.

Income stream:

A debt that is owed from one party to another. The future payment(s) are also known as cash flow instrument or a debt instrument.

Indemnification:

A promise to, under outlined circumstances, compensate for loss or damage.

Institutional lenders:

Banks (local and regional), savings and loan associations, mortgage companies, and other finance companies and commercial lenders.

Insurance-based income streams:

The receiving of cash flows from insurance companies. Insurance-based income streams can be paid out to individuals or businesses.

Intangible personal property:

Something of value which is not a tangible asset. Intellectual property is the most common type of intangible personal property (e.g. copyrights, trademarks, patents, etc)

Investment-to-value ratio:

A financial equation used to measure the security of a creditor’s position and the likelihood that a foreclosure would result in a recoup of the investment.

Invoice:

A debt instrument specifying the amount the customer owes for delivered goods or services. The trading and/or selling of invoices occurs in a type of financing called factoring.

Joint venture:

A contractual agreement which binds multiple people or business together for the purpose of a specific task, operation, or goal.

Lead:

Information which may be useful in a search for prospective clients.

Leverage:

The depth of an entity’s reliance upon borrowed money, this is measured by using the ratio of debt to total assets.

Liabilities:

The total amount owed (to all creditors), with the exception of ownership equity. Also see Current Liabilities and Long Term Liabilities.

Lien:

Liens are used tin the world of finance, and also in the justice system. It is the claim against a property by a creditor/a court.A lien is removed once the debt is paid/a court ruling is satisfied.

Lien Search:

Due diligence involving a thorough search to see if there are any claims against the property of a business or an individual. Main sources of information in a lien search are the County Clerk's and Secretary of State's offices.

Limited liability company (LLC) :

A legal structure for businesses which is designed to combine attributes of corporate and partnership structures.

Line of Credit:

An arrangement with a set total credit which may be extended by a lender to a specific borrower. Having a line of credit allows the client much more flexibility in that they can borrow up to that sum at any time, with little or no additional paperwork; this also is useful in planning operating expenses.

Liquidity/Liquid Assets:

A company a high level of liquidity if it has a lot of liquid assets. Liquid assets are easily converted into cash with little loss. The better liquidity a business/individual has, the better they will be able to meet their obligations in a timely fashion.

Loan-to-value ratio:

A ratio used to test how likely the owner of a property is to default, based on measuring how heavily mortgaged the property is.

Long Term Liabilities:

Debts which are due only after a year’s time. This is called funded debt, and will be found on a balance sheet in the Liabilities section.

Marginal credit customers:

Lenders who generally pay debt, but have some late/slow payment patterns.

Market value:

The current price that the educated, interested consumer would purchase something.

Mechanics Lien:

A lien on property (such as a building or an invoice) given to secure compensation to contractors and other workers involved in construction or other property improvement, A mechanics lien usually takes first precedence in the event of other liens on the same property.

Mortgage:

A contractual instrument which pledges real property as security for a debt. A mortgage is a type of lien.

Negative Cash Flow:

This occurs when total expenses exceed total income. In this situation, there are no profits, and increasing debt.

Note:

A written promise to pay. A note should include the amount, the name of the creditor and the date by which the money is promised.

Notice of Pre-lien:

A document provided by a contractor or provider of materials to the owner of real property, This notifies the owner that a lien against the real property will be sought if invoices for materials or services being provided for the improvement of the real property remain unpaid.

Notification:

In factoring, when an invoice is purchased from a client, the debtor on that invoice can be notified, and be asked to pay the factor directly.

Non-Notification:

In confidential factoring, notification does not occur, and the debtors on the purchased invoices remain ignorant that their debt has been purchased.

Non-Recourse Factoring:

In Non-Recourse Factoring, the responsibility for debt collection falls directly on the factor. If the customer is unable to pay off the debt, the loss is assumed by the factor.

Overhead:

Business costs which are unrelated to production or sale of goods or services. Some examples of overhead include office rent, a flat fee telephone line, or a company car. Overhead expense remains unchanged regardless of sales.

Owner financing:

In this arrangement, a.k.a. seller financing, the seller of tangible personal property accepts a promissory note in lieu of immediate payment of a portion or the entirety of the purchase price.

Partnership:

This is a legal business structure which is one of the most common. A partnership is legally similar to a Sole Proprietorship, except it involves joint ownership in a business.

Payee:

A person or business who is a creditor and is interested in selling his income stream for cash. In this glossary, the payee is generally referred to as the client.

Payor:

The entity who owes the debt on an income stream. In this glossary, this person is generally referred to as the customer or the debtor.

Personal guaranty:

This is the opposite of non-recourse. In this instance, the seller assumes personal responsibility and liability, effectively guaranteeing the income stream.

Portfolio:

A group of debt instruments which are all of the same type.

Pre-ship Invoice:

This is an invoice for services or goods which have yet to be delivered. indicating the amount due for which indicates the amount due from a customer to pay for goods or services which have NOT yet been delivered.

Privately held:

In factoring, this term is used to refer to debt which is owed to an individual or a business, as opposed to a financial institution.

Principal:

Generally, this term refers to the owner of a privately held business. However, during a financial transaction, the buyer and seller are both called principals.

Profit and loss statement:

This financial statement gives a historical view of an entity’s income and expenses.

Promissory note:

A writeen debt instrument which lists a specified amount promised to a particular party, to be paid over a outlined time period.

Purchase Order:

The document or form used to request goods or services.

Quantity Discount:

Any price reduction which is results from of purchasing in larger volume or bulk.

Rate of Return:

The return on an investor’s capital. Also called Yield.

Rebate:

The return of reserve funds to the client by a factor.

Recourse:

In recourse factoring, the client is liable to the factor, regardless of whether the customer pays or not.

Replevin:

A court action which occurs when the rightful owner or property is unable to retrieve it from the person holding the property. A factor might file to seize non-real estate property given as security for a defaulted debt.

Reserve:

This is money held by a factor as a form of guaranty. It is given to the in order to cover any defaults or other payment delinquencies. Any excess reserve is rebated to the client after the allotted time has elapsed.

Reserve Account:

A tracking method used by factors to invoices as they are paid and to track remaining invoices.

Satisfaction:

Satisfaction has occurred when the debtor has paid everything due, and the obligation is discharged.

Schedule of Accounts:

This report lists information on purchased accounts. It is provided by a factor to his client.

Seasoning:

How much time payments have been being made on a debt instrument.

Secondary market:

Privately held income streams can be sold by the owners for cash in the secondary market.

Security:

Assets given or promised to a creditor, so as to ensure that a loan is repaid..

Securitization:

The bundling and resale of income streams to investors, both private and public. This is regulated by the SEC.

Security interest:

An interest in non-real estate assets created under the Uniform Commercial Code (see below), This interest is given as security for an obligation.

Seller:

The entity holding a debt instrument, with a desire to sell it.

Servicing:

This includes administrative duties such as accounting, insurance, tax, payment collection and follow-up and loan analysis.

Sole proprietorship:

The legal business structure that is the default option for a small business. It simply means that a business is owned and operated by an individual. If a business fails to file for a different structure, they are automatically considered by the government to be a sole proprietorship.

Subordination:

This occurs when a creditor states in writing that the debt due to a different creditor has higher priority, than does debt owed to himself.

Tail:

The back half of the payment stream, when a separate entity has rights and interest in the first half. This is often a balloon payment.

Tangible personal property:

Tangible assets, excluding real estate (cars, jewelry, boats, etc)

Time value of money:

A financial concept regarding the differing value of money received today, versus in the future or past.

Title insurance:

Title insurance protects the beneficiary from suffering any damages due to real estate titling issues. This insurance can be issued to the payor or to the payee.

Title policy:

The policy which provides title insurance. Title insurance protects the beneficiary from suffering any damages due to real estate titling issues. A title policy can be issued to the payor or to the payee.

Trade Discount:

A discount in the event that payment is received by a certain date.

Trial balance printout:

A table listing the loans in a specific portfolio along with their payment schedule. Most portfolio transactions require a trial balance printout.

UCC-1:

The UCC Financing Statement is filed with the Secretary of State or the County Clerk's office. It is used by a factor to perfect a lien on a clients' accounts receivable.

UCC-2:

A UCC Statement with Respect to Change is filed with the Secretary of State or the County Clerk's office to provide evidence of an assignment, release or change in the UCC-1.

UCC-3:

This form is filed by a factor, in order to terminate a UCC- 1. It is filed when all outstanding invoices are paid.

Uniform Commercial Code:

This State Code regulates property transfers.

Unseasoned:

A lease or other long term debt with few, if any, payments made on it.

Verification:

In factoring, this is a step of the due diligence process in which the validity of an invoice is confirmed by the customer.

Yield:

The ratio of income over a specified period of time to the total cost over that time. Yield is a measure of the return on an investor's capital investment.

Behind every small business there is a business owner. We believe in business owners and we invest in their potential.